The Picking Problem: Why Retail Stores Make Terrible Warehouses

When you order from Instacart or a similar service, here's what actually happens: a gig worker drives to a retail store, walks the aisles with a shopping cart, searches for your items, deals with out-of-stocks, makes substitution decisions, waits in checkout lines, then drives to your home. The average pick time in a retail environment is 60-90 seconds per item. For a typical 30-item grocery order, that's 30-45 minutes just picking before the driver even gets in their car. Add drive time to the store (5-10 minutes)and delivery to your home (10-15 minutes), and you're looking at 55-80 minutes in a best-case scenario. Why so slow? Because retail stores are designed for browsing, not operational efficiency. Wide aisles, promotional endcaps, seasonal displays, all the things that make stores pleasant for shopping make them nightmares for rapid fulfilment. Dark stores flip this equation. Purpose-built warehouses with optimized layouts enable pick rates of 120-150 units per hour: that's 24-30 seconds per item. The same 30-item order takes 12-15 minutes to pick, leaving ample time for delivery within a 60-minute window.

The Inventory Black Hole

Marketplace apps have zero visibility into inventory until their shopper arrives at the store. This creates a cascade of problems:

- Out-of-stocks discovered mid-shop

- Customer service calls about substitutions

- Refund processing delays

- Terrible customer experience ("Why did I wait 90 minutes to learn you don't have my items?")

- They can't optimize inventory for their customers because they don't own it. They're at the mercy of whatever the retail partner has in stock, organized however that retailer chooses.

With vertical integration, quick commerce operators control their inventory end-to-end. We at GoDirect stock what our specific neighborhoods want: whether that's South Asian spices, Caribbean produce, or kosher items. Real-time inventory systems maintain 96%+ fill rates. Predictive ordering based on our own sales data means popular items rarely stock out.

The Math Doesn't Work: A Tale of Two Business Models

Marketplace Model (Instacart-style):

- Average order value: $100

- Revenue (25% take rate): $25

- Shopper cost (picking + delivery): $15-20

- Payment processing & support: $5

- Contribution margin: $0-5 (0-5%)

The marketplace model generates low single-digit contribution margins at best. They need massive order values or take rates so high they drive customers away. Many marketplace delivery companies lose money on every order and try to make it up on volume: a strategy that's failed spectacularly across the industry

Dark Store Model:

- Average order value: $70

- Revenue (35% retail margin): $24.50

- Pick cost (salaried picker, 15 min): $3.50

- Delivery cost (batched routes): $5

- Payment processing: $2

- Contribution margin: $14 (20%+)

Dark stores generate healthy contribution margins because they capture full retail margin and operate with warehouse-grade efficiency.

The Delivery Density Dilemma

Marketplace models suffer from scattered order patterns. A shopper might pick up an order in North Toronto, deliver to Scarborough, then get their next gig back in Mississauga. These "dead miles" kill economics and make consistent sub-60 minute delivery impossible during peak hours. Dark store networks solve this through geographic density. Each location serves a tight 4-24 km radius. All deliveries originate from one point. Drivers can batch 2-6 orders on a single route, return to the hub, reload, and repeat. Driver utilization hits 80%+ versus marketplace rates of 40-50%. This density advantage compounds: the more orders in a zone, the more efficient each delivery becomes. For marketplaces, more orders in peak hours mean longer wait times. For dark stores, more orders mean better batching and lower per-order costs.

Why Incumbents Can't (or Won't) Pivot

You might ask: "Why doesn't Instacart/Large Retail just build Dark Stores?". Here’s why:

- Cannibalization Risk:

- Instacart's marketplace generates GMV from partnerships with Loblaws, Costco, and other retailers. Operating competing dark stores would destroy these relationships.

- Innovator's Dilemma:

- When you have a $30B+ marketplace business, every strategic decision gets filtered through "How does this protect our core?" The answer is usually "Don't disrupt yourself."

- Organizational DNA:

- Marketplace companies are built around logistics and software. Retail operations, procurement, inventory management, merchandising require completely different expertise and culture.

- Capital Allocation:

- Building 100 dark stores requires $25M+ in Capex. For a marketplace platform, that's dead weight on the balance sheet compared to asset-light revenue growth.

The Failed Experiments Tell the Story:

- The quick commerce graveyard is full of well-funded corpses:

- Getir (Turkey, $12B valuation): Pulled out of North America entirely

- Gorillas (Germany, $3B valuation): Sold for parts after burning through billions

- Buyk (Russia): Shut down by DoorDash six months after acquisition

- Instacart's warehouse pilots: Quietly scaled back in most markets

These weren't execution failures. They were business model failures. Companies that tried to graft quick commerce onto marketplace infrastructure, or that competed on the same commoditized SKUs as supermarkets without differentiation, discovered that unit economics don't magically improve at scale.

Then there are success stories:

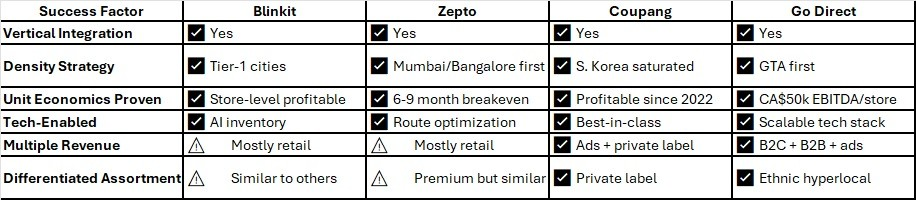

Blinkit:

- 700+ stores, acquired for $570M

- Store-level profitable in mature markets

- 3,000-5,000 orders/store/week in dense areas.

Zepto:

- $5B valuation, 500+ stores

- 40%+ Month 3 retention

Break-even in 6-9 months per store.

Coupang:

- $30B market cap, profitable since 2022

- 38% market penetration in South Korea

- 60%+ Month 6 retention.

Picnic:

- Profitable since 2021

- 80%+ Year 1 retention

<$5 CAC (organic growth).

Quick commerce has proven successful in multiple markets when done right. Blinkit and Zepto in India are store-level profitable with 700+ and 500+ dark stores respectively. Coupang in South Korea built a $30B company on vertical integration and density. Picnic in Europe has been profitable since 2021. And now Go Direct in Canada. What they all have in common: vertical integration, unit economics first, geographic density, and strong retention. What failed—Getir, Gorillas—all violated these principles by blitz-scaling before proving profitability.

What Actually Works: The Quick Commerce Playbook

Profitable sub-60 minute delivery requires several elements working in concert:

- Vertical Integration Own the entire stack from procurement to last-mile delivery. No middlemen, no take-rate negotiations, full control over customer experience.

- Hyperlocal Assortment Don't try to be everything to everyone. Serve specific communities with products they can't easily find elsewhere. In Toronto, that means deep ethnic SKUs. In Vancouver, different demographics drive different assortments.

- Dual Revenue Streams B2C retail margins alone aren't enough. Add B2B wholesale to restaurants and convenience stores, last-mile as a service for other retailers, in-app advertising, and data monetization. Multiple margin layers create defensibility.

- Efficient Expansion Each dark store should reach profitability within 12-16 months and then fund the next wave of expansion. This isn't a "raise billions and blitz the market" strategy. It's methodical market-by-market density building.

The Canadian Opportunity

Canada presents a unique opportunity for quick commerce to succeed:

- Weather Creates Demand Try schlepping groceries home in a Toronto February. Dark stores eliminate weather-related shopping friction: a genuine competitive advantage unavailable in temperate markets.

- Immigration Drives Density 500,000+ new immigrants annually, clustering in urban centers, creates exactly the population density quick commerce requires.

- Incumbent Weakness Canadian grocers are infrastructure-dependent oligopolies protecting legacy store networks. They won't disrupt themselves, creating a window for new entrants.

- Underserved Ethnic Communities 20% of Canadian grocery spend comes from ethnic consumers who are dramatically underserved by mainstream retailers. Whoever cracks hyperlocal ethnic assortment wins disproportionate loyalty.

What This Means for Retail's Future:

The death of quick commerce has been greatly exaggerated. What's actually happening is a Darwinian sorting process:

- Dying: Marketplace models trying to bolt speed onto fundamentally slow infrastructure

- Thriving: Vertically integrated operators with differentiated assortments and profitable unit economics from Day 1

The future of urban grocery retail isn't 50,000 square foot supermarkets or gig workers wandering Costco. It's networks of 2,000-4,000 square foot dark stores with warehouse-grade operations, serving tight geographic zones with exactly what those communities want, delivered in under an hour.

This isn't the future of all grocery retail. Suburban families will still do weekly shops at Costco.

But for urban consumers who want fresh produce tonight, ethnic ingredients for tomorrow's dinner party, or basics delivered between meetings: Go Direct fills that space seamlessly

The infrastructure to serve them profitably finally exists. And it looks nothing like the marketplace model that dominated the last decade.

Building Go Direct: Lessons Applied:

At Go Direct, we're building Canada's quick commerce super app with these principles at our core:

- 100 dark stores across Canada (company-owned and franchised)

- 2,000+ SKUs curated for diverse communities

- Sub-60 minute delivery with 30%+ contribution margins

- B2C + B2B dual revenue streams for defensibility

- Proven unit economics: CA$250k setup, CA$1M revenue, CA$50k EBITDA per store

- Want to connect? I'm always interested in conversations with:

- Investors focused on retail tech and quick commerce

- Operators who've scaled multi-site retail/logistics networks

- Strategic partners in real estate, procurement, or last-mile delivery

Reach me at arun@go-direct.app or connect here on LinkedIn.